Global air cargo rates continue their downward trajectory in July amid decreased volumes and increased capacity – foreboding a difficult winter season for airlines, as analyzed by Xeneta-owned CLIVE Data Services.

03 / 08 / 2023

According to chief airfreight officer at Xeneta, Niall van de Wouw: “The month of July rarely provides any surprises in terms of unexpected performance levels in the global air cargo market, but what will be concerning airlines and forwarders is the constant month-on-month decline in average rates, and the quickening pace of this fall since the turn of the year” .

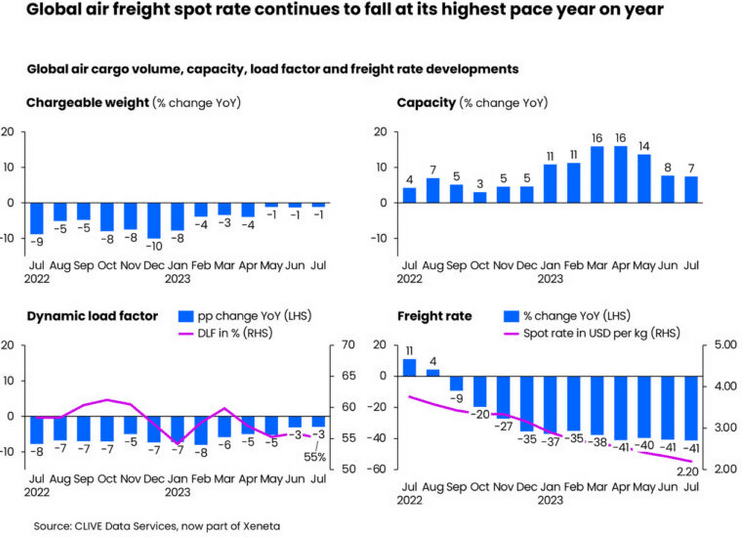

Month over month volumes of global air cargo slumped by 2% in July, while the general rate of cargo global airfreight spot saw a 40% drop or more for the fourth consecutive month.

July experienced a 7% capacity rise year on year while airlines stepped up summer schedules to accommodate passenger demand. This, coupled with the airfreight volumes nosedive, resulted in a tumble in the cargo load factor, which witnessed a drop by 3% compared to July 2022, although on a level with June 2023 at 55%.

July 2023 air cargo spot rate was $2.20 per kg on average, which saw a small drop from the previous month rate at $2.31 per kg, but a noticeable 41% downturn on July 2022.

The final week of the month saw a spot rate pickup, which reflected “an easing decline in cargo volumes and slower paced growth in capacity versus previous months”.

The increase may also have been due to the jet fuel prices upturn. However, CLIVE does not anticipate any long-term impact on rates from that quarter at this time.

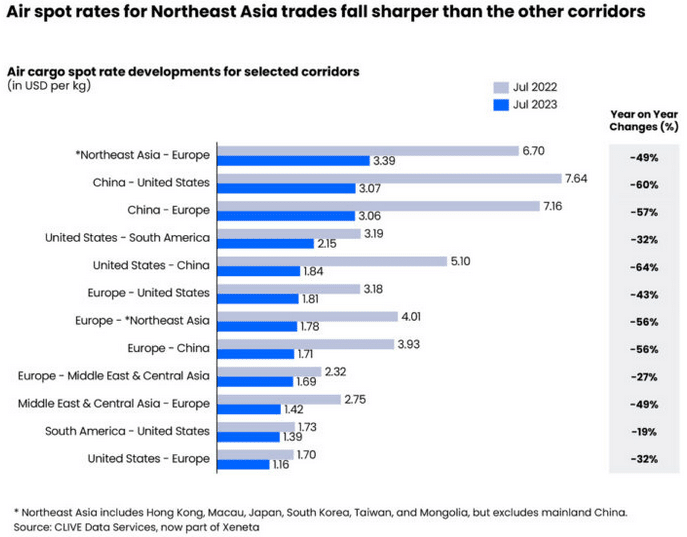

Among the trade lanes, Northeast Asia witnessed the biggest declines in the rate of transactions. This is corroborated by over 60% fall in China–US and US–China rates year on year, while China–Europe and Europe–China rates both saw a downturn of more than 55% compared to July last year.

CLIVE also reported the smallest year-on-year declines in the South America–US and Europe–Middle East and Central Asia by 19% and 27% respectively.

Van de Wouw further pointed to the critical winter rates negotiation period, stating that the shippers would likely have the upper hand. “We are already seeing more shippers relaunching contract negotiations with their logistics service providers to push down airfreight rates. Shippers are also looking to agree longer, 12-month commitments to reduce their costs. Airlines will know they can expect the same pricing turbulence from forwarders.”

With their Q2 air freight revenues seeing a year-on-year contraction of around 50%, freight forwarders such as Kuehne+Nagel, DHL Global Forwarding and DSV are seriously short for money.

Spot rates for this segment of year have gone below the seasonal rate since May 2022 due largely to the competition among forwarders to see higher yielding business in the general cargo market. However, ever since the outbreak of the Covid-19 pandemic, spot rates for special cargoes have remained above the seasonal rate.

“Those forwarders focused on grabbing volumes almost at any cost to increase their market share will continue to sacrifice their margins to do so, and likely continue to fuel an irrational air cargo market in which global spot freight rates fall deeper the level market fundamentals and conditions would typically expect,” cautioned CLIVE.

According to the company’s analysis, the Chinese manufacturing continuing decline and the decrease in new orders for Chinese exports will result in “muted” airfreight volumes for the rest of the summer.

“The airfreight rates merry-go-round will be intense this winter, as we have indicated in previous months’ analyses. Many freight forwarders, who at the peak of the pandemic chose multi-year contracts to secure airline capacity, are now reportedly bleeding cash, so they are under significant pressure to renegotiate rates which reflect the reality of today’s freight market and the expectation that the current market environment could continue for the foreseeable future into 2024”, concluded Van de Wouw.